1. What Is Open Banking and Why Should Businesses Care?

Open banking enables financial services to securely share financial data, such as balances and transactions, with regulated third-party providers via standardised APIs.

This unlocks new opportunities for fintech and financial institutions to improve customer experience, streamline payments, and increase cross-selling without increasing risk or complexity.

Why it matters for B2B:

- Data-driven financial insights: Businesses gain real-time visibility into cash flow, income, and expenses, which are critical for forecasting and decision-making.

- Faster, cheaper payments: Instant bank-to-bank payments eliminate card and intermediary fees, streamline receivables, and enable secure and reliable payments.

- Better access to finance: Using aggregated data, lenders can more accurately assess repayment capacity and credit risk, reducing friction and time to funding. Savings banks can assess affordability and offer relevant savings accounts.

2. How Does Open Banking Work? (Real-World Examples)

- AIS (Account Information Services) pull up-to-date account data.

- PIS (Payment Initiation Services) trigger direct bank-to-bank payments.

Real-World Examples:

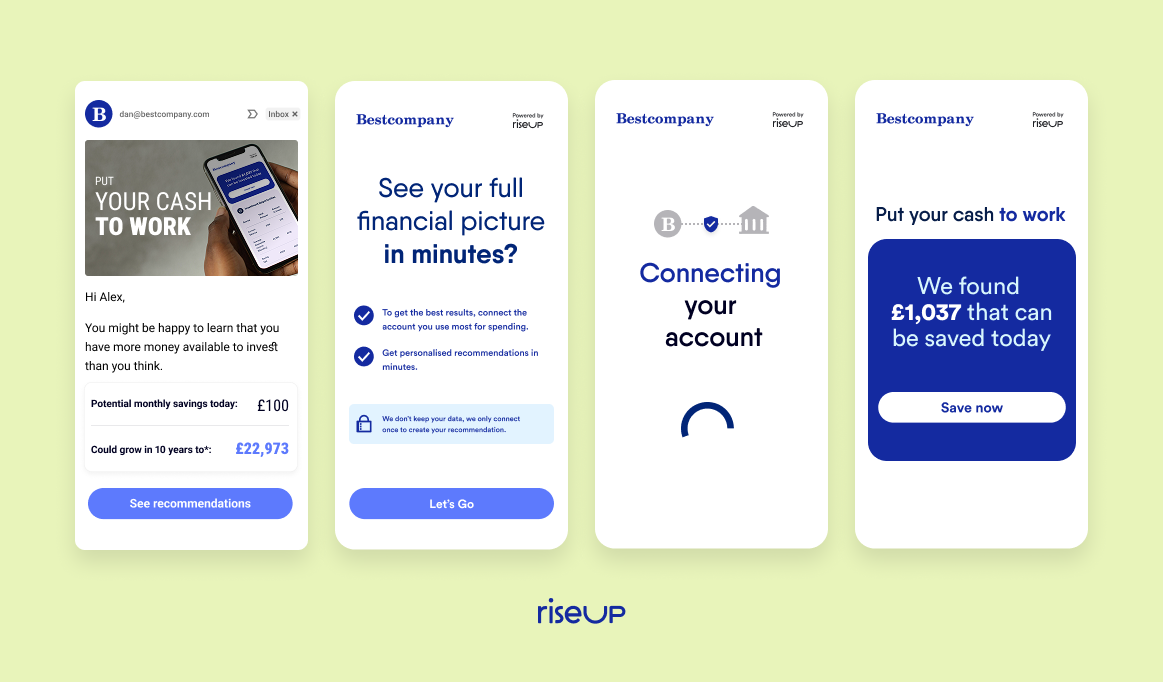

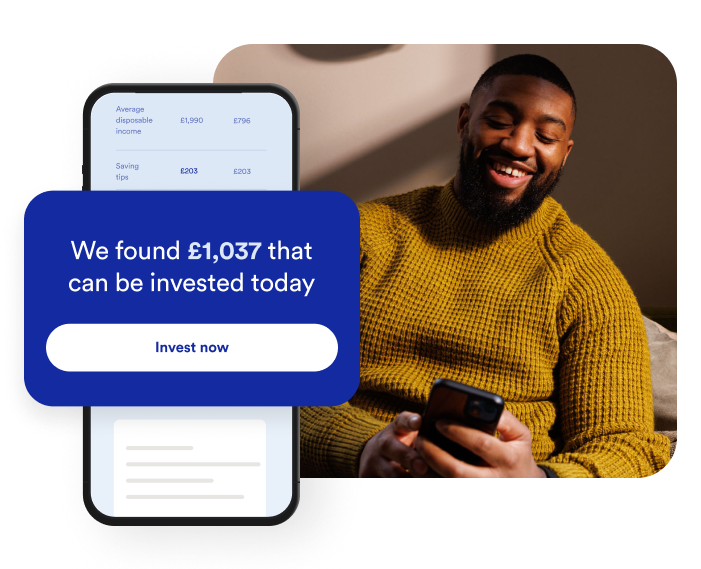

- RiseUp savings insights uses AIS data to detect disposable income and trigger automated savings nudges, helping people take action in real time.

- GoCardless’ instant bank pay enables frictionless, card-free payments, cutting fees and settlement times.

By mid‑2025, 13.3 million UK consumers and small businesses, around 1 in 5, use open banking services monthly, a 40% YoY increase. The ecosystem adds £4.1 billion in yearly economic value and supports nearly 5,000 jobs.

This strong foundation empowers businesses to automate invoicing, adopt VRP, and streamline supplier payments. It also sets the stage for embedded lending, real-time insights, and regulated scaling under PSD3.

3. What Are the Benefits of Open Banking for Businesses and Fintech Platforms?

Efficiency & Automation

- Business use case: Automate reconciliation, payroll, and recurring payments to reduce manual processes.

- Outcome: Lower operational costs and faster execution with fewer errors.

Real-Time Cash Flow Insights

- Business use case: Access real-time financial data to better understand customer behaviour and financial patterns.

- Outcome: Enhanced customer segmentation and more timely, relevant product recommendations.

Faster, Lower-Cost Payments

- Business use case: Enable instant bank-to-bank payments and remove reliance on card networks.

- Outcome: Reduced payment processing costs (by 54%) and faster settlement.

Smarter Credit & Lending

- Business use case: Assess affordability in real time and trigger relevant loan offers.

- Outcome: Higher loan uptake, reduced risk, and quicker credit decisions.

Enhanced Customer Experience

- Business use case: Deliver personalised insights and seamless pay-by-bank payment flows.

- Outcome: Increased engagement, higher conversion, and improved retention.

Cross-Bank Reach

- Business use case: Connect to multiple banks through a single integration.

- Outcome: Simplified scaling and access to richer customer data for existing and new customers.

Here are a few examples of how businesses are leveraging Open Banking + AI:

- Improve deposit reinvestment: When a customer’s deposit term ends, AI detects idle funds across accounts and prompts account reinvestment, boosting retention without raising interest rates.

- Increase loan uptake: Use real-time affordability insights to trigger tailored loan offers when customers are most likely to qualify, improving conversion and reducing default risk.

- Personalised financial nudges: AI spots moments like bonus payments or spending drops, and triggers timely nudges (e.g. savings prompts or investment top-ups) based on actual deposit capacity, not static segments.

4. How Is Open Banking Regulated and Implemented in the UK?

- PSD2 & UK Open Banking Standard mandated 9 largest banks to expose APIs starting in 2018.

- Security guardrails: Bank-level encryption, strong customer authentication, and a consent-based access model.

- Adoption stats: As of March 2025, 13.3 million UK users (~18 %) are actively using open banking across consumer and small business segments, a 40% increase year over year.

5. How Is RiseUp Using Open Banking + AI to Enhance Financial Services?

- Seamless data access: Securely connect to real-time customer financial data through regulatory-compliant Open Banking integrations.

- Payment initiation: Let customers pay and move money instantly with no friction and no manual steps.

- Accessible lending and credit: Real-time affordability checks using live data to pre-qualify customers seamlessly.

- AI-driven financial nudges: Leverage machine learning models to deliver hyper-personalised nudges at key financial moments via multiple channels.

- Seamless compliance: Built-in consent tracking, strong authentication flows, and audit logs to ensure regulatory alignment.

- Enriched customer segmentation: Enhancing customer data collection to support more accurate & relevant marketing efforts and rollout AI-driven financial strategies.

6. What Is the Future of Open Finance and Data‑Driven Financial Services?

- Open Finance: Data-sharing expands beyond current accounts into mortgages, pensions, investments, and insurance.

- VRPs (Variable Recurring Payments): Recurring payment innovation is growing, with 13 % of payments in March 2025.

- Next-gen regulation (PSD3): Coming in 2026, aimed at fraud reduction, enhanced consumer rights, and broader API coverage.

- AI-powered financial infrastructure: Predictive insights, real-time affordability, and personalised nudges at key financial moments are paving the way, with open data as the backbone.

FAQ

Yes. It uses bank-grade encryption and strong customer authentication (SCA). Data is only shared with user consent, and no sharing of login credentials.

Under PSD2 and the UK Open Banking Standard, regulated Third‑Party Providers access data only with explicit, renewable consent. Strong oversight applies.

By partnering with Open-Banking‑certified providers (e.g., banks, aggregators, fintech platforms like RiseUp), onboarding includes consent flows and security audits.

RiseUp integrates AIS and PIS to offer financial institutions and platforms to understand their customers’ revenue potential, provide real‑time consumer insights, and personalised consumer-facing solutions within a secure, compliant framework.

Next step

Fintech leaders who integrate Open Banking and AI today will define tomorrow’s financial engagement. Ready to unlock growth with smarter data?