Introduction: why open banking matters in 2025

Open Banking began as a compliance exercise. In the UK, PSD2 and the CMA Order required banks to share customer data securely through APIs. For years, this created charts and dashboards that showed people what they already knew, how much they spent on groceries or fuel, but delivered little action.

By 2025, the picture is changing. Open Banking has become a core financial infrastructure. It enables fintechs, banks, and investment platforms to access real-time financial data and turn it into smarter, more personalised offers and customer engagement.

- In March 2025, the UK had 13.3 million active open banking users, up 40% year on year (Open Banking Limited).

- That same month, customers made 31 million open banking payments, accounting for almost 8% of Faster Payments (Open Banking Limited).

- Adoption is accelerating worldwide, with markets such as the US (via CFPB 1033), Brazil (PIX), and India (UPI) building open finance ecosystems at pace.

The opportunity is clear. Open Banking is no longer about data access. It is about using that data to trigger the right offer at the right moment.

Key definitions you need to know

- Account Information Services (AIS): permissioned access to customer account and transaction data.

- Payment Initiation Services (PIS): third-party initiation of payments directly from a bank account.

- Consent: customer approval to share data with a trusted third party. Must be explicit, time-bound, and auditable.

- Strong Customer Authentication (SCA): two-factor security required for sensitive actions.

- Variable Recurring Payments (VRPs): the next generation of Direct Debit, allowing flexible recurring payments with customer-defined parameters.

The global perspective: regulation and adoption

United Kingdom and Europe

- The UK leads with one of the most advanced frameworks (PSD2, PSR 2017, Open Banking Implementation Entity).

- Open Banking adoption is mainstream, almost one in five UK consumers or SMEs with a current account actively used Open Banking in March 2025.

United States

- No single regulatory framework, but the CFPB’s Section 1033 rule is driving momentum.

- The market relies on aggregators such as Plaid, MX, and Akoya, but is moving toward standardisation.

Emerging markets

- African markets such as Nigeria are developing Open Finance standards to enable inclusion.

- Brazil’s PIX and India’s UPI showcase how open payment rails can achieve mass adoption rapidly.

Opportunities for fintechs and banks

1. Smarter savings

Detecting idle balances across accounts allows institutions to nudge customers into moving money into savings or ISAs. For example, after payday, a customer with £2,000 left untouched for 48 hours could be prompted to transfer £500 into a savings account.

2. Responsible lending

Cash-flow-based affordability checks reduce default risk. Real-time income and expense data provide more accurate underwriting than traditional credit scores.

3. Investment activation

Open Banking detects bonus payments or consistent surpluses and nudges customers to contribute to ISAs, pensions, or investment accounts at the right moment.

4. Embedded finance

Large purchases such as a car or home move can be detected through spending signals. This creates natural cross-sell opportunities for insurance, loans, or protection products.

Challenges and risks

- Security: API breaches and data misuse remain key risks. Providers must use bank-grade encryption and comply with GDPR and the UK Data Protection Act 2018.

- Consent fatigue: customers are unlikely to connect accounts without clear, immediate value. Intent-driven consent (“connect to find £300 in savings”) drives far higher uptake than generic requests.

- Fragmentation: global differences in API quality and regulation create friction.

- Commercial models: in payments, particularly VRPs, the industry still debates sustainable pricing models.

- Competition: many fintechs offer aggregation, but few deliver engagement that translates to measurable business outcomes.

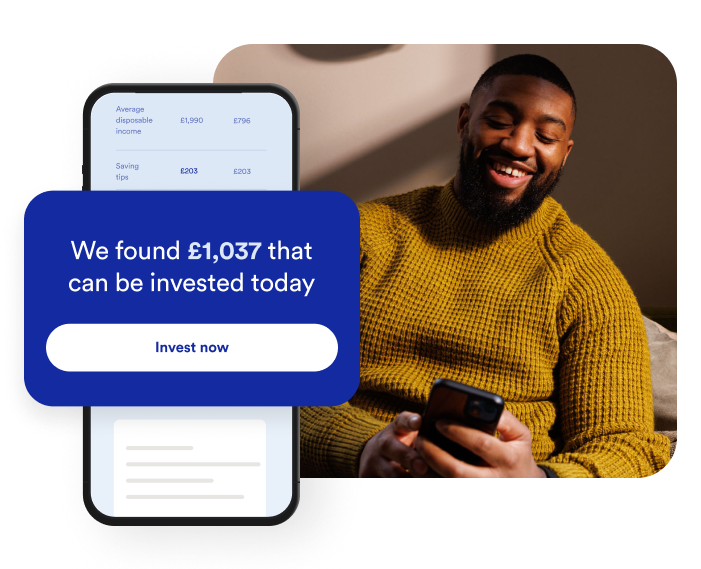

RiseUp’s lens: from data to action

At RiseUp, we believe the future of Open Banking is about turning financial data into action. Not dashboards. Not charts. Action.

As described by Ziv Tubin in his CTech interview, RiseUp’s Financial Insights Engine works through three layers:

- Detect financial signals: real-time financial indicators such as payday, idle balances, and spending patterns.

- Identify moments to engage: contextual life events when action is most relevant, such as days after payday, bill due dates, or deposit maturities.

- Personalised offers: pre-built engagement journeys that transform signals and moments into customer actions like deposits, reinvestments, loan uptake, or investments.

This approach allows institutions to move beyond static campaigns and instead engage dynamically at the point of customer intent.

Proof points from RiseUp’s partners:

- +25% uplift in deposit reinvestments.

- 40%+ consent rates for Open Banking data access.

- Average household disposable income uplift of £390/ month for RiseUp-connected users.

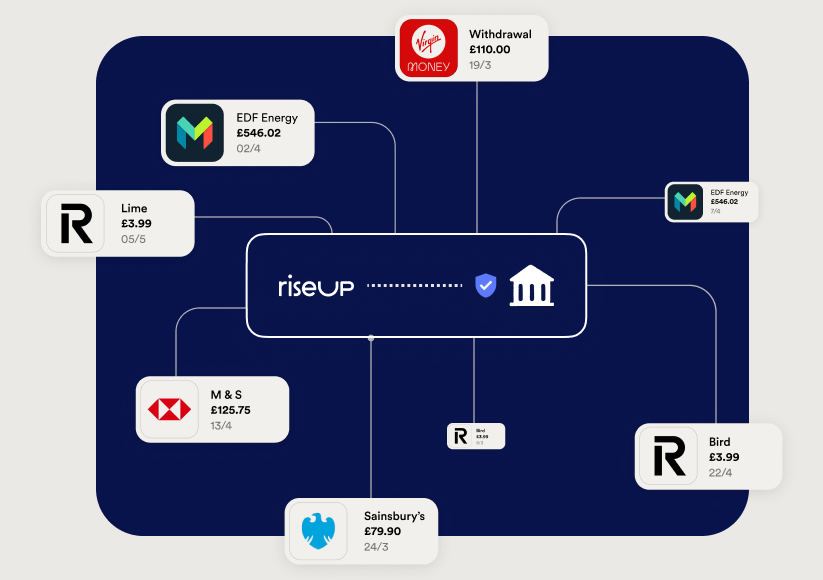

Visualising the flow

Frequently asked questions

What is Open Banking and how does it work?

Open Banking allows regulated third parties to securely access bank account data and initiate payments with customer consent. APIs provide the bridge between banks and fintech applications.

What are the main benefits for fintechs and banks?

It enables new products, better risk assessment, reduced acquisition costs, and higher engagement through personalised offers.

What risks should companies be aware of?

Security breaches, customer mistrust, fragmented regulations, and weak consent flows that fail to show clear value.

How is Open Banking regulated globally?

The UK and EU are the most advanced, with PSD2 and local regulations. The US is moving toward Open Finance through CFPB 1033. Emerging markets such as Brazil and India lead in payments adoption.

How does RiseUp use Open Banking differently?

Unlike dashboards that only display data, RiseUp’s Financial Insights Engine acts on real-time signals. It connects moments of financial readiness with personalised offers, delivering measurable revenue for partners while supporting customer wellbeing.

Conclusion: from compliance to competitive advantage

Open Banking has moved from compliance tick-box to competitive advantage. The winners will be those who act on signals in real time, turning data into deposits, lending, and investments.

RiseUp’s Financial Insights Engine is designed to help institutions capture these opportunities with minimal effort. It is a hosted, compliant, no-code solution that delivers impact within days, not months.

The question for financial leaders in 2025 is no longer whether to use Open Banking, but how quickly they can turn it into growth.