Introduction: Beyond Rates, Toward Trust

In 2025, the challenge for banks, fintechs, and financial institutions is clear: customers expect more than a headline rate. They want guidance they can trust, control over how they save, and proof that their institution has their best interests at heart.

Offering an extra 0.25% interest may catch attention, but it does not build loyalty. What does? Timely, personalised support that helps people make smarter financial decisions with AI saving tools for banks and fintechs and personalised deposit growth strategies.

63% of UK consumers now hold more than two bank accounts and 32% have switched in the past five years. Loyalty is fragile and switching costs are low. Institutions that fail to provide real value risk losing customers quickly.

How banks rely on traditional marketing to retain deposits

Recent headlines have highlighted how banks use generic campaigns that remind customers to retain deposits. This approach sometimes works, but it does not feel motivating for customers. It is not effective enough to build lasting trust, and it leaves institutions relying on costly tactics like raising interest rates to attract new deposits.

Why personalised saving nudges are more effective than generic deposit campaigns

Younger customers are looking for more. Among 25 to 34 year olds, 78% expect their bank to use AI for personalised advice and 84% think apps should provide more tailored insights. This group also has the highest idle balances, with 64% holding more than £2,500 in low or no interest accounts.

Customers are telling us what they want: actionable insights, not pressure.

-

Trust, not tricks. Customers want their bank or investment platform to guide them, not just sell.

-

Control, not commands. They want to decide how and when to act based on their data.

-

Confidence, not complexity. They want tools that make them feel financially secure, not overwhelmed.

When financial institutions only chase deposits, they risk disengaging their customers, the very audiences they need most.

RiseUp’s B2B2C model: AI for personalisation and growth

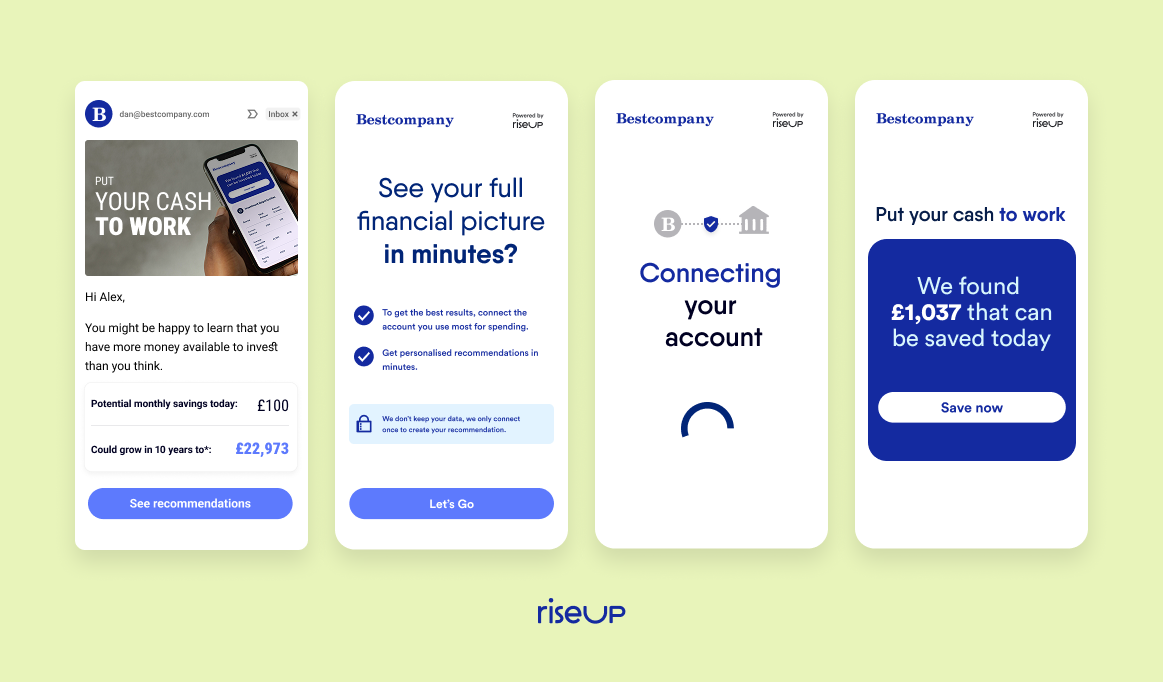

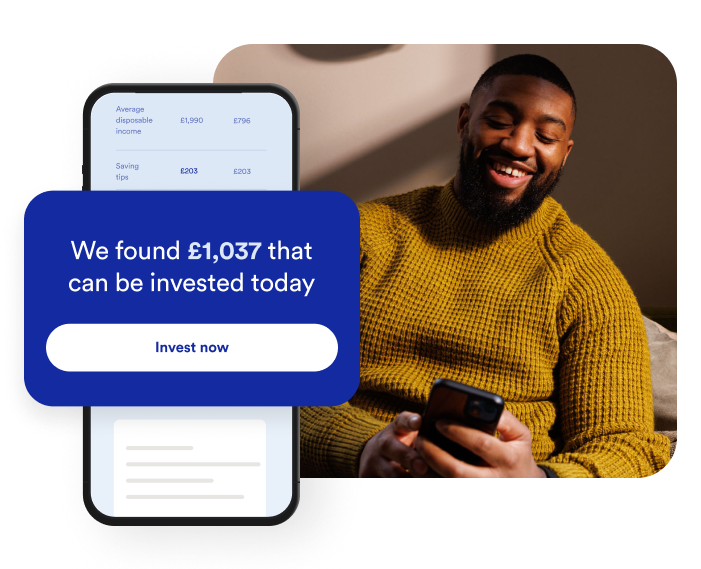

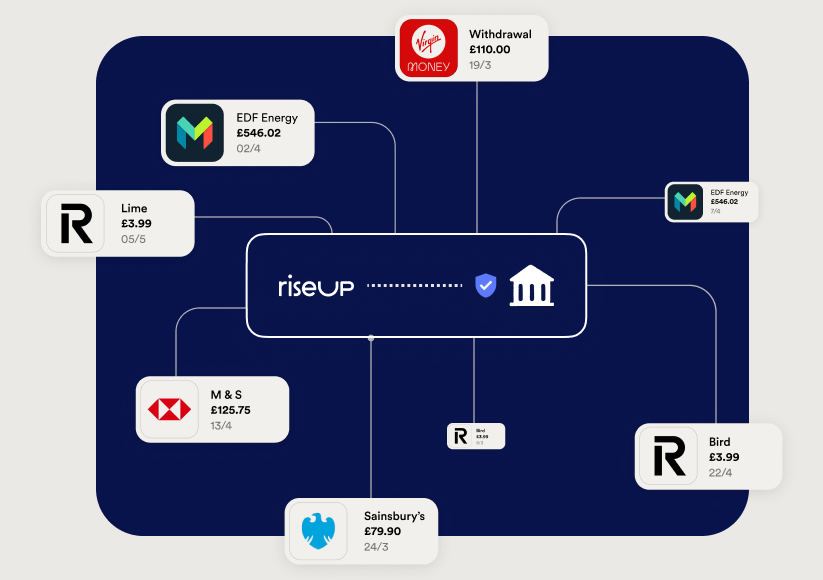

RiseUp was built for this new reality. Our Engagement Engine helps financial institutions, including banks, fintechs, investment platforms and credit unions, deliver AI-driven financial guidance into existing customer journeys.

-

Financial Signals detect real-time readiness, such as idle cash or income changes

-

Engagement Moments identify life events like payday, bill due dates, or deposit maturity

-

Pre-built Journeys guide customers into savings, investments, or repayments at exactly the right time

These flows are consent-first, FCA-compliant, and require no code or integration. Institutions can launch and test them in weeks and scale them quickly.

By aligning customer financial wellbeing with institutional goals, RiseUp creates a win-win model. Customers feel supported while institutions grow deposits, retention, and trust.

Value for financial institutions

-

Increased loyalty and trust: Position as a financial ally, not just a product provider

-

Higher engagement: Customers act on timely and personal nudges, not ignore them

-

Sustainable growth: More deposits and product uptake without relying on expensive rates or acquisition campaigns

Value for end-users

-

Personalised nudges based on real customers’ spending and income

-

Control: Customers choose when and how to act on offers

-

Confidence: Guidance that feels like personal insights, not a sales push

Case in action

A UK savings bank launched RiseUp-powered reinvestment and top-up journeys. Within 60 days, reinvestment rates increased by 25% and engagement grew by more than 40%. Customers saved more, while the institution reduced churn at deposit maturity.

These are not driven by abstract graphs and dashboards. They are actions customers take, and trust, because they feel informed and supported, not sold to.

FAQ: AI, trust, and smarter personalisation

How can AI help banks and fintechs retain deposits under Consumer Duty?

AI personalisation tools for banks and fintechs detect financial signals like idle cash and payday. Then, they deliver personalised deposit growth strategies that protect customers based on affordability while driving retention.

What is B2B2C financial wellbeing?

B2B2C financial wellbeing means financial institutions deliver personalised nudges and offers to help customers achieve financial goals through a partner like RiseUp, which benefits both customers and institutions.

How does RiseUp partner with financial institutions to serve customers?

RiseUp helps its partners deliver no-code CRM campaigns and branded flows that seamlessly fit into existing customer journeys. It uses Open Banking data and AI to trigger timely, personalised offers.

Why do younger users respond better to guidance than sales tactics?

Younger customers expect AI personalisation and authenticity. Guidance feels supportive and builds trust, while sales pushes feel transactional.

What differentiates RiseUp’s AI from other Open Banking tools?

Unlike other Open Banking providers, RiseUp creates rich customer profiles and powers CRM campaigns with pre-built journeys that detect customers’ financial signals and key engagement moments, converting them into actions that improve wellbeing and business KPIs.

Conclusion: The early-movers advantage

The future of banking engagement is not about pushing higher rates or one-off campaigns. It is about helping customers feel in control of their money and offering personalised deposit growth strategies that deliver measurable growth for financial institutions.

RiseUp’s AI enables exactly that. In 2025, the institutions that adopt this model will not just win more deposits or loans, they will win customer loyalty for the long term.

For a deeper look, explore our AI powers smarter personal finance stories or read the FCA’s view on the Targeted Support regulation, considered a once-in-a-generation change.