Why lenders and brokers need personalisation?

The UK’s housing market faces a growing affordability challenge. A recent TimeOut analysis highlighted London as an extreme example: in Kensington & Chelsea, a household needs almost £200,000 in annual income to buy, while in Barking & Dagenham, it is closer to £60,000.

For financial institutions, the question is not only how to serve the households that already qualify. It is how to help the much larger segment of aspiring buyers get financially ready faster, while generating more qualified leads, stronger engagement and higher conversion.

What challenges stop first-time buyers in the UK?

-

Large deposits needed: With UK house prices, first-time buyers often need £100K or more just for the deposit. For many households, that feels out of reach. For lenders, this also limits the pool of qualified applicants and makes it harder to guide customers toward deposit engagement schemes or savings accelerators.

-

Mortgage limits: Even if people are earning well, lenders usually cap borrowing at about 4.5 times salary. That rules out a big share of potential buyers and also limits the lender’s ability to highlight alternatives, such as shared ownership, deposit boosters or government schemes.

-

High funnel drop-off: Generic tools like calculators fail to engage prospects until they are already ready to transact.

-

Delayed engagement: By the time buyers approach a lender or broker, many have already chosen a competitor.

How can AI personalisation help lenders and brokers?

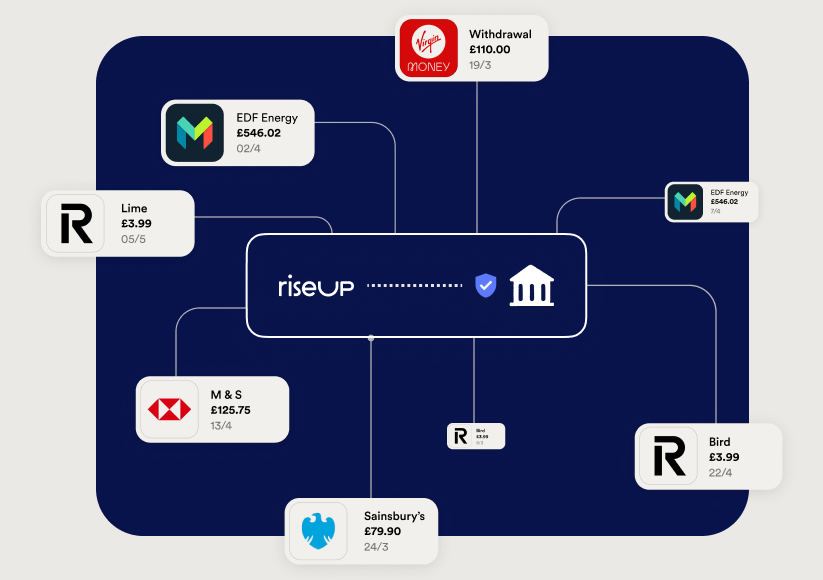

Generic calculators and static campaigns no longer build pipeline. Behaviour-based personalisation, powered by Open Banking and AI, gives lenders and brokers new ways to capture, nurture and convert leads earlier:

-

Lead capture at scale: Offer monthly cashflow insights to your entire audience, building trust and visibility before customers are mortgage-ready.

-

Signal detection: Identify the cohorts showing consistent saving behaviour, reduced debt or stable disposable income, the leading indicators of affordability.

-

Personalised engagement: Deliver targeted nudges and cross-sell offers when customers cross financial readiness thresholds.

-

Plug-and-play journeys: Deploy pre-built engagement flows that trigger based on affordability signals, guiding customers through steps such as building a downpayment, choosing the right mortgage type, or getting ready to buy once their deposit goal is achieved.

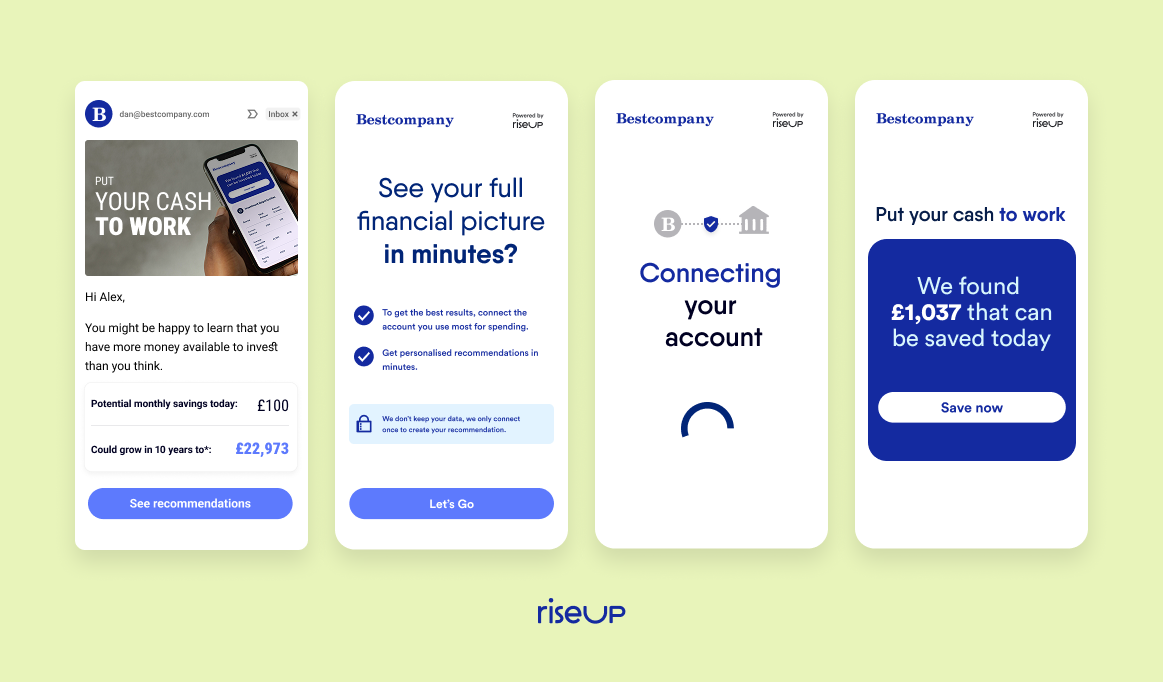

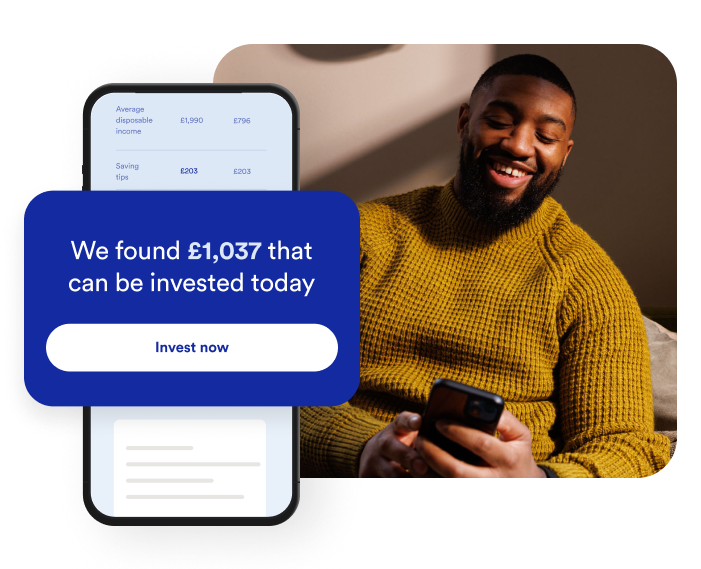

What does affordability insights look like in practice?

In Islington, the average property costs £658,700, requiring a 15 to 20% deposit of £100K to £132K. By contrast, in many UK regions outside London, average house prices are lower, but the principle is the same: affordability depends not only on income, but on consistent saving behaviour and the ability to optimise cashflow.

Imagine your platform already knows which customers are saving £1,400 per month. With monthly insights, you detect an extra £360 per month available by reallocating discretionary spend. This accelerates the deposit timeline by 15 months.

Instead of waiting for these customers to approach a broker or bank, your system proactively engages them with a personalised offer, building loyalty and capturing the mortgage lead before competitors do.

This is how you shift from static calculators to continuous engagement journeys.

How can mortgage brokers use AI to generate more leads?

Brokers often rely on inbound enquiries. AI personalisation creates an outbound engine that delivers:

-

Top-of-funnel reach: Send monthly deposit or affordability trackers to your whole CRM base.

-

Segmentation that matters: Detect which cohorts are approaching readiness and focus resources on them.

-

Conversion uplift: Engage when customers are financially able to act, improving lending uptake.

-

Plug-and-play journeys: Roll out pre-built flows across your CRM, automatically nurturing leads with personalised steps such as building their downpayment, exploring mortgage types, or preparing to buy once their savings goal is achieved.

For brokers, this means moving from waiting for leads to actively creating a steady flow of high-intent prospects.

Why AI personalisation matters to your KPIs

For decision makers across mortgage, deposit, partnership and marketing teams, personalisation means measurable business impact:

-

More qualified leads entering the funnel

-

Higher deposit growth through activation of idle savings

-

Improved lending uptake by engaging customers at the right financial moment

-

Better retention and loyalty by providing continuous engagement to customers on their journey to home ownership

This is not just about helping first-time buyers. It is about creating a B2B2C growth engine that ties customer engagement directly to your organisation’s revenue outcomes.

What is the opportunity for lenders and brokers?

The UK’s affordability gap will not close overnight. But lenders and brokers can turn this challenge into a competitive advantage.

By deploying AI and Open Banking personalisation, you can:

-

Capture leads earlier, when customers first set affordability goals

-

Engage them with ongoing value, not just one-off calculators

-

Convert them into long-term customers when readiness is clear

The winners will be the institutions that act now, building personalised, readiness-based engagement while competitors are still relying on generic campaigns. Those that move first will own the next generation of mortgage customers.